Secure Act 2.0 Updates

You may have heard in the news that the Secure Act 2.0 was passed right before New Year’s. As always, we try to be proactive and notify you of any changes that could impact your financial plan. Listed below are some of the most notable changes within the new legislation and if you have any questions, feel free to reach out on how these changes could impact you directly!

Please be aware that there isn’t clear guidance yet for changes in 2024 & 2025, but we will continue providing updates as we get more information on the implementation of the new rules.

For Young Adults & Pre-Retirees:

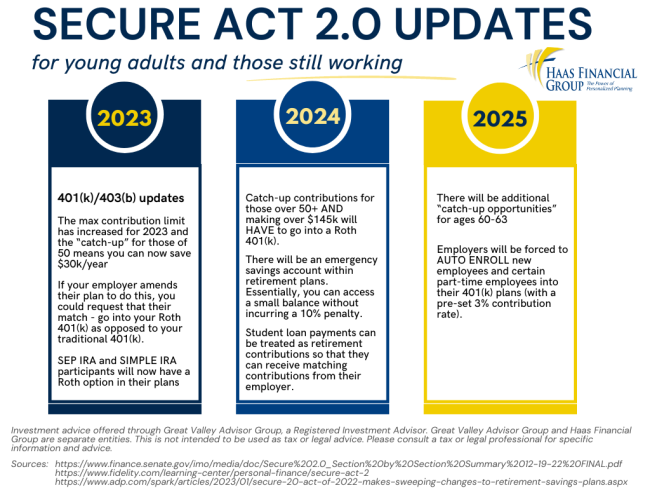

- 401(k)/403(b) updates in 2023 include:

- The max contribution limit has increased to $22,500 in 2023 and the catch-up contribution for people age 50 and over increased to $7,500 (up from $6,500 in 2022). Total maximum contribution of $30k per year for people age 50+.

- Employers are now able to amend their plans and allow employees to dictate if they want employer matching and non-elective contributions to be made as Roth contributions. There is more guidance expected on this updated rule (previously any employer contributions had to be made as a pre-tax contribution)

- NOTE: if you elect to receive your employer match or non-elective contribution as a Roth contribution, that amount will be included in your taxable income for tax purposes.

- In 2024, changes include:

- Any catch-up contributions for those that are age 50+ and earning more than $145k per year will have to be made as a Roth contribution.

- NOTE: Previously, you could make your catch-up contribution pre-tax to reduce your taxable income. If you fall into this specific circumstance, your catch-up contributions will have to be made as Roth, meaning you’ll pay the income taxes now on your catch-up contributions but will be able to access them tax-free in the future.

- Student loan payments can be treated as retirement contributions so that they can receive matching contributions from their employer. Employers will make contributions to the plan on behalf of employees who are paying off their student loans instead of saving for retirement, but it’s expected that there will be an annual verification process to certify the amount of qualifying student loan payments

- NOTE: This will be up to the employer to offer this as it won’t be a requirement for them to implement. In the case that the employer offers this assistance, if an employee chooses not to contribute to their 401(k) but makes student loan payments, the employer can make “matching contributions” to the employee’s retirement plan based on their student loan payment amounts. This is to help employees get savings into their retirement account.

- There will be an emergency savings account tied to retirement plans (save up to $2,500 in Roth contributions annually)

- Withdrawals from this account will not incur any penalties

- Separately, participants are entitled to an Emergency Withdrawal of up to $1,000/year without incurring the 10% early withdrawal penalty beginning in 2024

- Any catch-up contributions for those that are age 50+ and earning more than $145k per year will have to be made as a Roth contribution.

- Lastly, updates in 2025:

- Participants age 60-63 will have the opportunity to contribute $10k per year (indexed for inflation) as the annual catch-up contribution

- NOTE: This is an increased amount compared to the catch-up contribution for people age 50-59 ($7,500/yr) and will be subject to the same Roth rules for anyone making more than $145k annually.

- Employers will automatically enroll eligible participants into their 401(k) and 403(b) plans and have the default contribution rate of at least 3% and will have an annual auto-escalation of 1%, not to exceed 15%. All current plans will be grandfathered

- Part-time employees (working between 500-999 hours) for 2 consecutive years must be allowed to participate in their company’s retirement plan (previously was 3 years)

- Participants age 60-63 will have the opportunity to contribute $10k per year (indexed for inflation) as the annual catch-up contribution

- SEP & SIMPLE IRA Updates:

- You will now have the ability to contribute on a Roth basis to your SIMPLE IRA and will be able to elect Roth employer contributions in your SEP IRA

- Note: if you elect to receive your employer contribution as a Roth contribution, that amount will be included in your taxable income for tax purposes

- You will now have the ability to contribute on a Roth basis to your SIMPLE IRA and will be able to elect Roth employer contributions in your SEP IRA

For Retirees:

- RMD updates taking effect in 2023 include:

- The RMD age has been raised to 73 (previously 72). If you have already begun taking your RMD last year or previously, this update doesn’t affect you

- People will only have a 25% income tax penalty for not taking their full RMD (previously was 50%) and can be further reduced to 10% if the missing distribution is corrected within 2 years

- In 2024:

- Roth 401(k)s will become exempt from RMDs. This only applies to people who choose to not roll over their Roth retirement plan into a Roth IRA

- In 2033:

- The RMD age will be raised to age 75

- The annual IRA charitable distribution limit of $100,000 will be indexed for inflation moving forward. The Act will also allow a one-time gift of $50,000 from an IRA to a charitable trust or charitable annuity and allow the one-time gift to be treated as a qualified charitable distribution (QCD).

- NOTE: QCDs are a great way for charitably inclined people to meet the RMD rules and allows them to avoid income taxes as the money is sent directly from their IRA to the charity, charitable trust, or charitable annuity.

- A surviving spouse of a participant who passes before taking their RMD will now be allowed to elect to be treated as the employee for RMD purposes. This is to delay when the RMD would begin

- NOTE: This would be beneficial in the case of a couple with a large age gap and in the scenario where the younger spouse passes first. For instance, if a couple were ages 75 and 60 and the 60-year-old passes, the 75-year-old spouse may choose to elect to treat the deceased’s retirement account as their own, but not actually roll the funds into their own retirement account. This would delay the RMDs beginning until the deceased spouse would have turned the RMD age (currently age 73) instead of beginning in the year the spouse passed away because the beneficiary is age 75.

General Knowledge for All Age Groups:

- A rising concern among people saving for college is having excess money in their loved one’s 529 plan. An update in this legislation will allow people to roll over 529 college savings plan to a Roth IRA penalty-free beginning in 2024. The rollover amount is limited each year to the Roth contribution limit and has a lifetime rollover limit of $35k. 529 plans must also be opened for over 15 years before you are eligible to move funds to a Roth IRA.

- NOTE: This is beneficial to a loved one not going to college or not using all the funds within the 529 plan. If you choose to roll the money over into a Roth IRA, you must remember that the amount moved must be within the annual Roth contribution limit ($6,500/yr in 2023) and any contributions made to the 529 within the last 5 years (and the earnings on those contributions) are ineligible to be moved to a Roth IRA.

- The Department of Labor will be creating an online database in the next 2 years called the “Orphaned Account Database,” which will help employees and employers find orphaned retirement accounts and help match them to current retirement plans

- NOTE: This is to help people with a few small 401(k)s from previous employers from becoming “lost” over time. Once found, you will be able to roll over the funds into an IRA or your current retirement plan.

Sources:

https://www.fidelity.com/learning-center/personal-finance/secure-act-2

Links to additional resources not referenced in this article:

https://www.lpl.com/newsroom/read/insider-blog-top-10-provisions-in-the-new-secure-2-act.html

Investment advice offered through Great Valley Advisor Group, a Registered Investment Advisor. Great Valley Advisor Group and Haas Financial Group are separate entities. This is not intended to be used as tax or legal advice. Please consult a tax or legal professional for specific information and advice.

Tracking # T005354